It’s 9:47 AM on a Monday at a mid-size private bank branch in Gurugram. The branch manager has already lost the morning. Four customers are waiting to update KYC details on dormant accounts. A relationship manager is searching through three different systems to gather a loan applicant’s history before a 10:30 AM call. None of this is the kind of urgent that makes headlines. It’s the kind of urgency that quietly burns out good people; that’s why Agentforce in banking has moved from a slide in a Salesforce pitch deck to real conversations at the branch level. Agentforce in banking isn’t just about chatbots anymore. It’s about whether a bank can keep its promises to customers when its employees are stretched thinner every quarter. The more closely you examine how Agentforce in banking is currently deployed, the clearer it becomes that this is less about technology and more about the workforce.

The Reserve Bank of India’s own 2023-24 Trend and Progress report makes that case in cold numbers: private sector banks now employ more people than public sector banks, yet their attrition has climbed sharply, averaging around 25% in recent years. People are leaving banking roles faster than banks can train replacements, and the work that once spread across a stable team now lands on whoever’s still at the desk.

The 39% Problem Nobody Talks About

Here’s a number worth sitting with: across financial services globally, advisors, bankers, and insurance brokers spend just 39% of their time on direct client engagement, with the rest lost to administrative work. Six in every ten working hours for people whose entire job is relationships go toward paperwork, system-switching, and chasing data that already exists somewhere in the bank’s own servers.

It’s not that bankers don’t want to spend time with customers. But they usually get time-crunched when their core banking system that doesn’t talk to the CRM and they have a compliance checklist to fill before the conversation even starts. McKinsey projects the US insurance industry alone will be short of 100,000 advisers by 2034, retiring talent and rising demand outpacing the hiring pipeline. The BFSI industry is watching a similar mismatch play out, precisely the opening Agentforce in banking is being built to fill.

This is the honest case for AI agents in banking operations, more honest than “AI saves money.” It isn’t about replacing the branch manager who knows her regulars by name. It’s about giving her back the 61% of her day that paperwork currently swallows!

Where the Machine Stops and the Human Starts

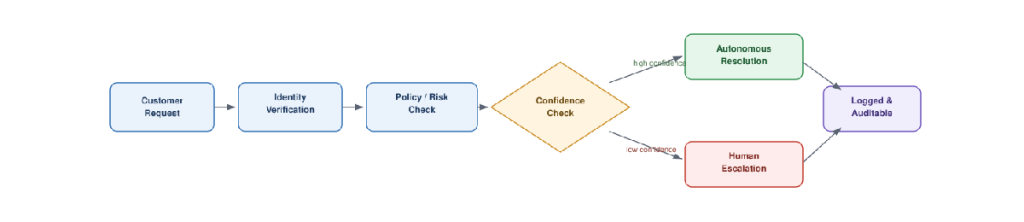

Many banks first think: “Wouldn’t it be possible for everything to be handled end to end in a single system. That’s not how serious deployments work. Salesforce’s own AI Operations Chief said it plainly earlier this year: large language models reason and communicate well, but as processes get more complex, their ability to reason consistently can start to waver, which is why solid architecture leans on deterministic, rule-bound execution wherever accuracy matters, and keeps the language model for flexible, conversational work.

In plain terms, an agent needs clear boundaries about what it decides alone and what it hands off. Here’s that escalation logic mapped out for a routine Agentforce in banking interaction:

This is the part most explainers skip, and it’s the part that decides whether a deployment succeeds. Banks that treat governance as an afterthought either over-trust the agent and create compliance exposure, or under-trust it and get none of the efficiency gain. The ones seeing real results build the escalation logic first and layer automation on top.

What Actually Changes on the Ground

Numbers from early adopters give a sense of what’s realistic, not theoretical. Crypto platform Nexo reported that agentic automation freed up 400 hours in a single quarter by autonomously managing routine inquiries, hours that went straight back into handling complex client needs. Absa’s relationship banking division saw sharper results still: its service team now resolves pressing customer issues 88% faster, while fraud management speeds up through round-the-clock agentic support.

Imagine that Gurugram branch manager’s Monday with such a system in place:

– KYC update requests get sorted the moment customers walk in, with verification already completed because the agent checked records against the core banking system overnight.

– The relationship manager preparing for the 10:30 AM call enters with one auto-generated summary instead of three open tabs, as the agent has already pulled together account history, repayment patterns, and risk alerts into one concise overview.

– Every action is logged and governed by the same compliance rules that guide her decisions, and it can be reversed by a human at any point.

That’s the difference between automation that creates risk and automation that minimizes it.

Agentforce posted 330% year-on-year growth in annual recurring revenue, crossing 500 million dollars in a single quarter, and more than half of new bookings came from existing customers buying more capacity rather than first-time buyers. Pilots that don’t work don’t get expanded budgets.

The Guardrail Is the Point, Not the Obstacle

There is a growing discussion happening in banking AI circles about accuracy. Salesforce’s leadership has reported that agent accuracy typically falls in the low-to-mid 90s percent range for production deployments. In many software fields, that figure is strong. However, in banking, where one incorrect fee reversal or misplaced KYC decision carries significant regulatory impact, 93% accuracy means that roughly one in every fourteen interactions still requires a human to address it. This is not a criticism of the technology but a reason for the layered, human-in-the-loop approach described earlier, instead of simply activating Agentforce in banking and walking away banks getting genuine ROI split the work this way:

– The agent handles the repeatable cases that used to eat a morning: routine KYC checks, fee reversals, balance queries, document verification.

– The banker handles the rare case that genuinely needed a human anyway, now with full context and the time to actually do it well.

– The remaining margin of error isn’t treated as a flaw to apologise for, but as the precise reason a banker’s judgment still belongs in the loop.

This is also where data quality advances from being an IT issue to a board-level concern. An agent’s effectiveness is only as good as what it can access. If KYC records, transaction histories, and loan applications exist in three disconnected systems, no prompting will solve that issue. Banks that properly implement Agentforce in banking fix their data organisation first.

Building This Without Breaking Anything

None of this happens by flipping a switch on a Friday and going live Monday. Institutions seeing real numbers, the 400 saved hours, the 88% faster resolutions, got there through a deliberate sequence:

- – Clean and connect the underlying data first, before any agent goes live.

- – Define exactly where Agentforce in banking can act independently versus where it must escalate.

- – Run it on one narrow, well-scoped use case before expanding to others.

- – Keep a human in the loop for anything carrying regulatory weight.

This sequence is where many in-house attempts fail, and it’s where an experienced implementation partner proves its worth, not by offering a magical AI solution, but by mapping a bank’s actual workflows, compliance limits, and core systems before deploying any agents. That’s the approach TechMatrix Consulting has taken with its Salesforce practice for BFSI clients across India, Asia, and the Middle East. They deploy Agentforce in ways that acknowledge the regulatory responsibilities of banking while freeing teams from the admin work that currently consumes their time. If your bank is past the question of “should we” implement Agentforce in banking, and is now focused on “how do we do this correctly,” that’s the conversation worth having next!